Financial advisor marketing is high-value lead generation inside a regulated category. A strong campaign has to attract qualified prospects, explain the advisory firm's value, respect financial-promotion rules, pass platform review and avoid misleading claims. That is a much narrower lane than ordinary B2B or local-service marketing.

The useful metric is not cost per lead. It is cost per qualified prospect, booked consultation, held consultation, onboarded client and client value. That value may be assets under management, annual advisory fees, planning fees or another internal measure depending on the business model. A low-cost download from someone outside the service model is not equivalent to a qualified household, business owner or retiree who becomes a long-term client.

This article is marketing guidance, not legal, compliance or financial advice. Financial advisory firms should review campaigns with qualified compliance counsel or internal compliance teams before launch, especially when ads include investment performance, testimonials, endorsements, retirement claims, tax planning, insurance, lending or jurisdiction-specific promotions.

TL;DR

- Financial advisor marketing should start with compliance. SEC/FINRA, state rules, FCA rules or other local regulations can shape claims, testimonials, endorsements, disclosures and recordkeeping.

- Platform rules add another layer. Google requires financial-services verification in some locations and expects financial-services advertisers to comply with local regulation and provide required disclosures.

- No campaign should imply a specific investment result. Strong advisory marketing sells process, clarity, specialization, fiduciary care where applicable, and education - not outcome certainty.

- Google and Meta play different roles. Google Search captures active intent; Meta usually works better for education, webinars, content, retargeting and trust building.

- Lead magnets are not the final conversion. Downloads, webinar registrations and quiz completions should be treated as early-stage events until qualification and consultation data are available.

- CRM feedback must protect privacy. Ad platforms should receive safe conversion statuses and values, not detailed financial records or sensitive client notes.

Why Financial Advisor Marketing Is Different

Financial advisory marketing is difficult because it combines regulation, platform scrutiny, trust and long sales cycles.

| Trait | Marketing implication |

|---|---|

| Regulated communication | Claims, testimonials, endorsements, performance data and disclosures need review |

| Trust-heavy decision | Prospects compare credentials, process, reputation, specialization and fit |

| High potential lifetime value | Acquisition cost should be judged against qualified clients, not raw leads |

| Slow conversion path | Content, webinars, consultations and nurture often come before onboarding |

| Sensitive personal data | Tracking must avoid sending detailed financial information to ad platforms |

| Platform verification | Financial-services advertisers may need approval before ads serve in some locations |

The funnel is closer to regulated professional-services marketing than ordinary lead generation. The firm is not selling an impulse purchase. It is asking someone to trust an adviser with money, retirement, estate planning, business exits, tax-aware planning or family wealth decisions.

Compliance First: The Practical Marketing Boundary

Compliance requirements depend on jurisdiction, registration status and the exact services promoted. A US SEC-registered investment adviser, a state-registered adviser, a broker-dealer, a UK adviser under the FCA perimeter, an insurance-led practice and a financial-planning firm can all face different rules.

Still, the practical marketing boundary is consistent:

| Area | Safer marketing posture |

|---|---|

| Investment returns | Avoid promises, cherry-picked outcomes and unbalanced performance claims |

| Testimonials and endorsements | Use only with required disclosures, oversight and recordkeeping |

| Third-party ratings | Explain basis, conflicts and selection criteria where required |

| Risk and limitations | Present benefits with fair treatment of material risks or limitations |

| Fiduciary language | Use only when accurate for the firm, account type and service |

| Specialization claims | Substantiate credentials, designations and niche expertise |

| Tax or legal language | Avoid individualized advice unless the firm is authorized and the context is appropriate |

| Financial urgency | Avoid fear-based, vulnerability-based or misleading pressure tactics |

The SEC's investment adviser marketing guide explains that the Marketing Rule contains general prohibitions against false or misleading advertisements, requires fair and balanced treatment in several areas, and sets conditions for testimonials, endorsements, third-party ratings and performance information. FINRA Rule 2210 governs communications with the public for member firms and includes approval, review and recordkeeping requirements for retail communications. In the UK, the FCA states that financial promotions should be fair, clear and not misleading.

That means campaign QA should cover ads, extensions, landing pages, webinar slides, lead magnets, emails, videos, retargeting copy and sales follow-up language. Compliance is not only a landing-page footer.

Google Ads For Financial Advisors

Google Search is valuable because it captures intent. A person searching for "financial advisor near me," "retirement planning advisor," "wealth manager for business owner" or "inheritance financial advisor" is closer to an advisory conversation than someone passively scrolling social media.

Useful campaign themes:

| Search intent | Example searches | Landing page need |

|---|---|---|

| Local advisor | financial advisor near me, wealth manager [city] | credentials, location, process, consultation CTA |

| Retirement planning | retirement planner, retirement advisor | education, planning process, suitability disclaimers |

| Business owner planning | financial advisor for business owners, exit planning advisor | niche expertise, business-owner proof, consultation path |

| Life events | inheritance planning advisor, divorce financial planner, widow financial planning | sensitive language, process, professional fit |

| Wealth management | investment management firm, private wealth advisor | service model, minimums where relevant, disclosures |

| Brand | firm name, adviser name, reviews | direct consultation path and reputation proof |

Google's financial products and services policy requires advertisers promoting financial products or services to comply with local law and provide required information such as business address, fees and proof of affiliations where asserted. Google's financial-services verification policy also states that verification is mandatory in some locations and may require information about services, licenses, registration numbers and business details.

Search campaigns should not launch before these basics are handled:

- correct advertiser identity and verification status;

- jurisdiction-specific landing pages where needed;

- clear business address and contact details;

- service descriptions that match registrations and permissions;

- visible disclosures and fee context where required;

- no misleading return, performance or risk claims;

- no unsupported credential or superiority claims;

- conversion tracking that does not pass sensitive financial details.

Meta Ads: Education And Retargeting, Not Hard Selling

Meta can be useful for financial advisors, but usually not as a hard-sell channel. The strongest role is education: guides, webinars, video explainers, retirement checklists, business-owner planning content, tax-season planning reminders and retargeting.

Effective Meta use cases:

- promoting a retirement-planning webinar;

- distributing a planning checklist or guide;

- retargeting website visitors who read service pages;

- nurturing content readers toward a consultation;

- building familiarity with adviser bios, process and client fit;

- supporting local seminars or events where compliant.

The creative should avoid language that implies knowledge of a person's financial condition, vulnerability or fear. Instead of "Worried you will run out of money?" a safer direction is "A planning session for retirement-income decisions." Instead of "Get higher returns," use process-oriented language such as "Review portfolio alignment, tax considerations and retirement income planning with an adviser."

Meta policies and enforcement can change, and some financial-services or credit-related promotions may fall under special review, category or targeting restrictions. The campaign should be reviewed inside the current Meta Ads policy environment before launch. If the offer touches credit, lending, housing, employment, insurance or sensitive personal attributes, the review should be especially careful.

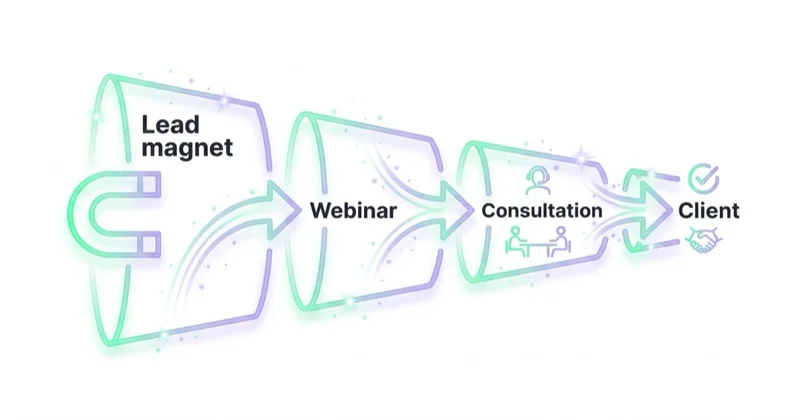

Lead Magnets, Webinars And Consultation Funnels

Financial advisor marketing often works best when the first conversion is educational. The prospect needs confidence before an introductory call.

Common funnel assets:

| Asset | Best use | Main risk |

|---|---|---|

| Retirement checklist | early-stage planning audience | generic download with weak qualification |

| Webinar | education and authority | low show rate without reminders |

| Tax-year planning guide | timely demand and email nurture | crossing into tax advice if not reviewed |

| Business-owner guide | high-value niche positioning | broad entrepreneurs with no planning fit |

| Portfolio review offer | closer to consultation | performance or suitability claims need care |

| Seminar / event | local trust and relationship building | compliance review of slides and follow-up |

The offer should match the firm's service model. A firm that works with business owners should not optimize toward generic retirement downloads. A fee-only retirement specialist should not buy broad "investment tips" traffic. A wealth management firm with minimum account requirements should qualify early enough to avoid filling the calendar with poor-fit conversations.

Landing Pages And Disclosures

Landing pages should be clear enough for users, compliance reviewers and platform reviewers.

Important elements:

- who the firm serves;

- what services are offered;

- where the firm is authorized or registered to operate;

- adviser or team credentials;

- fiduciary status where accurate;

- fee model or consultation expectations where appropriate;

- investment-risk and limitation disclosures where required;

- testimonial, endorsement or rating disclosures where used;

- privacy and data-handling information;

- a clear consultation or webinar CTA;

- no hidden risk language behind a tiny footer link.

The page should avoid broad performance, wealth, safety or superiority claims. Even when a phrase is technically defensible in one context, it can still create platform review friction or regulatory risk if not framed carefully.

For conversion structure, the general landing page fundamentals still apply: message match, proof, clarity, mobile usability and a single next step. In financial advice, the additional layer is fair, balanced and reviewable communication.

Qualification: What Makes A Prospect Worth Pursuing

Not every lead is a fit. Qualification should happen in a way that respects privacy and avoids sending sensitive details to platforms.

Useful internal qualification signals:

| Signal | Why it matters |

|---|---|

| Service need | retirement, investment management, tax-aware planning, business exit, inheritance, estate coordination |

| Jurisdiction / location | confirms whether the firm can serve the prospect |

| Client type | individual, household, business owner, executive, retiree |

| Fit with service model | AUM, planning fee, subscription or project engagement |

| Timeline | active need, future planning, event-driven urgency |

| Consultation status | booked, held, no-show, unqualified, referred out |

| Onboarding status | client accepted, declined, pending, lost reason |

Some firms use investable asset ranges or minimum fee thresholds as qualification criteria. If collected, that information should be handled carefully and generally kept inside CRM or secure intake systems, not sent to ad platforms in detailed form. Platform feedback can usually use safer status events such as qualified prospect, consultation booked, consultation held and client onboarded.

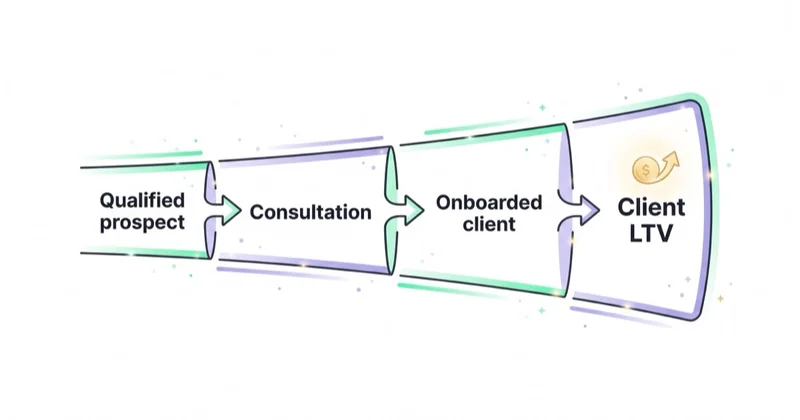

Measurement: Clients And Client Value

The most dangerous dashboard in financial advisor marketing stops at cost per lead. A cheap download can look efficient while producing no qualified consultations. A more expensive Search lead can be profitable if it becomes a client.

A practical measurement ladder:

- Ad click or paid social engagement.

- Content view, guide download, webinar registration or phone call.

- Qualified prospect.

- Consultation booked.

- Consultation held.

- Proposal, plan or next-step agreement.

- Client onboarded.

- AUM, annual fee, planning fee or estimated client value.

- Retention or expansion where available.

Google offline conversion imports and enhanced conversions for leads are designed for situations where an ad starts an offline sales path. For financial advisors, that can mean importing safe downstream events such as qualified prospect, consultation held or client onboarded. The event should not include sensitive financial records, account details, portfolio holdings, notes from advice meetings or personally sensitive context beyond what is required and permitted for measurement.

Value-based reporting can be useful, but it should use clean and compliant value proxies. Examples include estimated annual fee, first-year revenue band, client tier or approved value category. The goal is to teach media which campaigns produce qualified business, not to expose client-specific financial records.

Channel Roles In The Advisory Funnel

Each channel should have a job.

| Channel | Best role | Better KPI |

|---|---|---|

| Google Search | active demand for advisor, retirement or wealth-management help | qualified consultation rate |

| Meta | education, webinar demand, retargeting and familiarity | qualified registrations and assisted consultations |

| business owners, executives and professional niches | target-account engagement and qualified calls | |

| SEO | durable authority and service-page trust | organic consultations and assisted conversions |

| Email / CRM | nurture, show-up improvement, event follow-up | booked and held consultations |

| Referrals / partnerships | trust transfer from professional networks | referred consultations and client acceptance rate |

Comparing all channels by first-touch lead cost is misleading. Search may be more expensive but closer to consultation. Meta may create earlier-stage education. LinkedIn may reach a small but high-value niche. Email may turn a webinar attendee into a held consultation months later. The CRM should preserve that context.

Privacy And Tracking Guardrails

Financial data is sensitive. Tracking should be designed with the same seriousness as creative compliance.

Practical guardrails:

- do not send account balances, portfolio details, debt details, tax details or meeting notes to ad platforms;

- avoid passing sensitive form fields into URLs;

- avoid remarketing segments that reveal sensitive financial status;

- use consent and privacy notices appropriate for the markets served;

- hash first-party identifiers only where allowed and configured correctly;

- use conversion statuses rather than detailed financial facts;

- review server-side tracking and CRM integrations with compliance and legal teams;

- document which events are shared with each platform.

For technical implementation, enhanced conversions, server-side tagging and Meta Conversions API can improve measurement only if the data layer is designed properly. Better tracking is not a reason to send more sensitive information than necessary.

Space Ads Operating Approach

At Space Ads, regulated, high-LTV lead generation starts with constraints before channels. For financial advisors, that means understanding the firm's registration context, compliance review process, target client profile, service model, fee logic and CRM stages before campaigns are rebuilt.

The practical sequence is:

- Map compliance constraints and platform verification requirements.

- Define the qualified prospect: service need, jurisdiction, client type and economic fit.

- Separate Search intent by local advisor, retirement, wealth management, business-owner planning and brand.

- Use Meta primarily for compliant education, webinars, retargeting and nurture.

- Build landing pages with clear disclosures, service fit and trust signals.

- Track consultations and onboarded clients instead of only downloads.

- Feed safe CRM statuses and value proxies back into reporting.

When an account already spends but cannot prove which campaigns produce qualified consultations or onboarded clients, a marketing audit is the right starting point. Broader growth planning can sit under a fractional CMO engagement, while channel execution connects Google Ads, Meta Ads, content and CRM feedback.

30-Day Action Plan

- Days 1-3: run compliance discovery. Identify jurisdiction, registration status, review owner, disclosure requirements and platform verification needs.

- Days 4-6: define qualified prospect criteria. Service need, location, client type, timeline, economic fit and disqualifying factors.

- Days 7-10: audit landing pages and offers. Remove misleading claims, clarify disclosures, review testimonials and confirm privacy language.

- Days 11-14: rebuild conversion tracking. Separate downloads, registrations, booked consultations, held consultations and onboarded clients.

- Days 15-18: structure Google Search. Split advisor, retirement, wealth, business-owner, life-event and brand intent.

- Days 19-23: build compliant education funnels. Lead magnets and webinars should feed nurture, not stop at registration.

- Days 24-27: review Meta and retargeting policies. Check creative, targeting, category restrictions and personal-attribute risk.

- Days 28-30: evaluate by qualified pipeline. Compare cost per qualified prospect, held consultation and onboarded client by source.

Common Mistakes

| Mistake | Better approach |

|---|---|

| Promising returns or outcomes | Market process, fit, planning clarity and expertise |

| Treating disclaimers as a footer afterthought | Design pages to be fair, balanced and reviewable |

| Optimizing to lead-magnet downloads | Optimize toward qualified prospects and consultations |

| Uploading overly detailed financial data | Send safe status events and value proxies only |

| Ignoring financial-services verification | Confirm Google requirements before launch |

| Using fear-based retirement copy | Use neutral, educational language |

| Running testimonials without review | Apply required disclosures, oversight and recordkeeping |

FAQ

What is financial advisor marketing?

Financial advisor marketing is the process of attracting qualified prospects for advisory, planning or wealth-management services while staying inside regulatory, platform and privacy requirements. It usually combines Search, education, webinars, retargeting, SEO, email nurture and consultation tracking.

Can financial advisors advertise on Google?

Yes, but financial-services advertisers must comply with Google Ads policies, local laws and disclosure requirements. In some locations, Google requires financial-services verification before ads can run or target users seeking financial services.

Can financial advisors use Meta Ads?

Meta can be useful for education, webinar promotion, retargeting and lead magnets. Creative and targeting need careful review because financial products, credit-related offers, personal attributes and sensitive claims can trigger policy issues. The strongest Meta funnel is usually educational, not a hard-sell consultation ad.

Can financial advisors use testimonials in ads?

In the US, the SEC Marketing Rule permits testimonials and endorsements only when the adviser satisfies specific conditions, including disclosures, oversight and recordkeeping. FINRA, state rules, FCA rules or other local requirements may also apply depending on the firm. Testimonial creative should be reviewed before launch.

How should financial advisor marketing be measured?

Measure qualified prospects, booked consultations, held consultations, onboarded clients and client value. Cost per lead is too shallow because downloads and inquiries vary widely in fit. Safe offline conversion feedback helps platforms learn from downstream outcomes.

What should financial advisor ads avoid?

They should avoid outcome certainty, misleading performance claims, fear-based copy, unsupported superiority claims, unclear testimonial disclosures, hidden risks and language that implies knowledge of a person's private financial condition.

In Short

Financial advisor marketing works when compliance, education, trust and measurement are designed together. Google Search can capture active demand, Meta can educate and retarget, and CRM feedback can show which prospects become real clients.

The strongest accounts do not optimize to cheap downloads. They define a qualified prospect, use careful claims, complete required verification, protect financial privacy and measure consultations and onboarded clients with safe downstream conversion data.

Sources and further reading

- SEC - Investment Adviser Marketing

- FINRA - Rule 2210: Communications with the Public

- FCA - Financial promotions and adverts

- Google Ads Help - Financial products and services policy

- Google Ads Help - Financial Services Verification

- Google Ads Help - About offline conversion imports

Continue learning

Continue reading

Wedding Venue Marketing: Tours, Dates and Signed Bookings

Wedding venue marketing should fill the calendar with qualified tours and signed bookings, not just raw inquiries. This guide covers Google Search, Google Business Profile, wedding marketplaces, Instagram, Pinterest, galleries, off-peak dates, CRM follow-up and measuring tour-to-booking value.

Catering Marketing: Google Ads, Meta and Booked Events

Catering marketing works when event catering, corporate accounts and drop-off orders are measured separately. This guide covers Google Search, Meta, marketplaces, food trust, seasonality, quote quality and booked-event value.

Tree Service Marketing: Storm Leads and Booked Jobs

Tree service marketing has to capture emergency storm demand and steady planned work without wasting crew capacity. This guide covers Google Search, Local Services Ads, Google Verified, storm budgets, safety proof, call triage and cost per booked job.