Mortgage Lead Generation sits at the intersection of high-value sales, long consideration cycles, regulated financial advertising and fast follow-up. A mortgage lead is not valuable because a form was submitted. It becomes valuable only when the person is eligible, reachable, in the right market, matched to the right loan scenario, comfortable with the lender and eventually connected to an application and funded loan.

Google and Meta play different roles in that system. Google captures active demand from people already searching for mortgage options, refinancing, loan types or a local loan officer. Meta creates and reactivates demand among people who may be earlier in the process. Both can work, but they should not be measured or followed up the same way.

This guide explains how to build mortgage lead generation around intent, compliance, speed, CRM feedback and funded-loan economics rather than raw lead volume.

TL;DR

- Google and Meta create different lead types. Google Search captures active demand; Meta is better for education, retargeting, lead capture and audience warming.

- Loan type matters. FHA, VA, jumbo, DSCR, non-QM, first-time buyer, refinance and self-employed borrower searches should not be treated as one generic mortgage campaign.

- Compliance is part of performance. Google requires financial-service advertisers to follow applicable local regulations and provide required disclosures; Meta requires special handling for financial, housing and credit-related ads.

- Rate claims need strict review. Mortgage ads and pages should avoid unclear teaser language, missing terms, misleading payment claims or unsupported affiliation cues.

- Follow-up speed changes channel quality. Meta leads are often earlier-stage and need structured nurturing, while Search leads often need fast human intake and loan-scenario routing.

- The real KPI is funded-loan cost. Cost per lead is useful only when connected to application rate, qualification rate, funded loans and loan value.

Why mortgage lead generation is harder than ordinary lead gen

Mortgage lead generation has four structural challenges.

First, intent varies widely. Someone searching "VA lender near me" is in a different stage than someone clicking an educational Meta ad about first-time buyer steps. The same form field can hide very different readiness levels.

Second, the product is regulated. Mortgage advertising can involve rate, APR, fee, term, licensing, fair-lending and platform-policy requirements. Marketing teams need review workflows before campaigns go live, especially when rates, payments, affordability or government programs are mentioned.

Third, the sales cycle is long. A lead may move through first contact, qualification, document collection, application, pre-qualification or pre-approval workflow, property search, underwriting and funding. A campaign cannot be judged fairly if reporting ends at the first form fill.

Fourth, follow-up quality determines whether leads convert. A strong ad account can still fail when leads sit in an inbox, calls are missed, loan scenarios are not recorded and CRM stages do not flow back to the marketing team.

Google vs Meta: different demand, different handling

The channel strategy should start with intent.

| Channel | Demand type | Strong use case | Main risk | Better KPI |

|---|---|---|---|---|

| Google Search | active search intent | loan-type and local intent capture | broad generic terms and expensive weak clicks | qualified application or funded-loan cost |

| Google Performance Max / Demand Gen | mixed intent and remarketing | remarketing, audience expansion, creative testing | weak conversion signals | qualified lead value and CRM feedback |

| Meta lead forms | passive or early-stage demand | first-time buyer education, refinance interest, retargeting | low-intent volume without follow-up | contacted and qualified lead rate |

| Meta landing-page campaigns | consideration and education | content, calculators, guides, webinars | slow pages and weak disclosure review | scheduled call or completed application |

| SEO and local visibility | durable trust and research demand | loan-type pages, local pages, education | thin content and generic advice | organic qualified inquiries |

The most common error is comparing Google and Meta only by cost per lead. Meta may produce cheaper form fills because it creates earlier-stage demand. Google may produce fewer leads at a higher cost because it is closer to active intent. The useful comparison is downstream: contact rate, qualification rate, application rate, funded-loan rate and loan value.

Google Ads for mortgage leads

Google Search should be built around loan scenarios and local intent rather than generic "mortgage" traffic. Broad terms can attract research, calculators, definitions, rate shoppers, competitors, job seekers and people outside the eligible market. The account needs segmentation before bidding becomes meaningful.

Useful campaign themes include:

- loan type: FHA, VA, USDA, jumbo, DSCR, non-QM, conventional, reverse mortgage where allowed and reviewed;

- borrower scenario: self-employed borrower, first-time buyer, investor, second home, high-balance loan, credit-event recovery where policy and compliance allow the language;

- transaction type: purchase, refinance, cash-out refinance, rate-and-term refinance;

- local intent: loan officer, mortgage broker, lender or mortgage advisor by city or service area;

- program education: down payment assistance, first-time buyer programs, VA eligibility, investor financing;

- brand and referral protection: brand terms, partner names and competitor strategy separated for budget clarity.

Google recommends grouping Search keywords into related themes. In mortgage campaigns, that means every ad group should align with a specific borrower scenario, loan type or local intent and send traffic to a matching landing page.

Negative keywords should protect the budget from jobs, salary, training, calculators without lead intent, definitions, rate history, servicing support, complaints, payment login, free templates, unrelated credit products and states or markets outside licensing coverage. The negative keyword process should be reviewed weekly while new themes are being tested.

Meta for loan officers and mortgage brokers

Meta is rarely a pure substitute for Search. It is stronger for education, retargeting, lead magnets, early-stage buyer journeys, refinance awareness and list-based nurturing where consent and platform rules allow it. The creative should not imply that the advertiser knows a person's financial situation, credit status, income, debt level, family status or homeownership status.

Useful Meta angles include:

- first-time buyer planning guides;

- refinance decision frameworks;

- VA or FHA education without outcome promises;

- local market webinars with real estate partners;

- checklist downloads;

- retargeting after mortgage calculator, loan-type or guide page visits;

- testimonial or review creative after compliance approval;

- loan-officer introduction videos focused on process and trust.

Meta's Advertising Standards state that advertisers running financial products and services, housing or employment ads in the United States, Canada or certain European locations must self-identify as a Special Ad Category as available and use permitted targeting options. Meta also says ads for loans and insurance services must target people 18 or older and must not directly request certain financial information in the ad.

That changes campaign design. Mortgage Meta campaigns should rely less on narrow demographic assumptions and more on strong creative, broad but compliant audiences, landing-page education, CRM follow-up and conversion feedback.

Compliance and disclosure review

Mortgage advertising cannot be treated like ordinary service advertising. The review process should cover platform policy, lending regulations, licensing requirements and brand-specific compliance standards.

Google's financial products and services policy says advertisers promoting financial products and services must comply with state and local regulations for targeted locations and include required disclosures. Google also requires financial-product disclosures to be clearly and immediately visible rather than hidden behind hover states or separate tabs.

For mortgage campaigns, common review areas include:

- business name, physical address and licensing information where required;

- NMLS or equivalent licensing details where required by jurisdiction;

- rate, APR, payment and fee language;

- whether a rate is fixed, variable, introductory or conditional;

- whether taxes, insurance, points or fees are included in examples;

- government program references and affiliation language;

- refinancing, loan modification or foreclosure-prevention claims;

- fair-lending and non-discrimination requirements;

- privacy and consent language on forms;

- retention of materially different ads, pages and scripts where required.

The eCFR version of Regulation N lists prohibited mortgage advertising representations, including material misrepresentations about rates, APR, fees, taxes and insurance, prepayment penalties, variability of terms, government affiliation, source of the communication, approval likelihood and refinancing or modification claims. In practice, this means every rate or payment example should pass a strict compliance review before launch.

This article is marketing guidance, not legal or compliance advice. A lender, broker or loan officer should use internal compliance review and jurisdiction-specific counsel where needed.

Landing pages for mortgage lead generation

Mortgage landing pages have two jobs: convert interest and reduce unqualified intake. A generic form is not enough when eligibility, licensing, product fit and consumer understanding matter.

A strong mortgage page should include:

- exact match to the ad theme or loan scenario;

- licensed entity and contact details where required;

- clear scope of the product or service;

- plain-language explanation of the process;

- compliant disclosure placement;

- what information is needed for the next step;

- what happens after the form is submitted;

- privacy and consent language;

- phone and calendar options;

- loan-officer bio or team credibility signals;

- content reviewed for rate, APR, payment and government-affiliation language.

Forms should be useful without requesting unnecessary sensitive information in the ad environment. Early-stage forms can ask for transaction type, timeline, property state, loan purpose and preferred contact method. Deeper financial details usually belong in a secure application process, not in a casual social lead form.

For conversion quality, landing page strategy should connect directly to CRM stages. A page that creates many low-fit leads can look good in Google Ads and bad in the loan officer's calendar.

Follow-up and lead handling

Speed matters, but the bigger point is process. Mortgage follow-up should not rely on manual inbox checks. Leads should route automatically into a CRM or loan-origination workflow with clear ownership, source tagging and next-step logic.

A practical follow-up system includes:

- immediate notification to the assigned loan officer or intake team;

- phone, text and email sequence cleared through compliance review;

- different sequences for Search, Meta, referral and organic leads;

- stage labels for contacted, unreachable, qualified, not eligible, application started, application submitted, funded and lost;

- source and campaign fields preserved from the ad platform;

- opt-out handling and consent records;

- appointment scheduling and reminder flows;

- manual notes for loan scenario, market, timing and objection.

Meta leads generally need more nurturing because they are often earlier-stage. Google Search leads often need quicker scenario routing because they may be comparing lenders in real time. The same CRM can handle both, but the messaging and SLA should differ.

Call tracking is especially important when phone calls are a major conversion path. It should be implemented in a privacy-conscious way and evaluated by qualification and application outcome, not by call count alone.

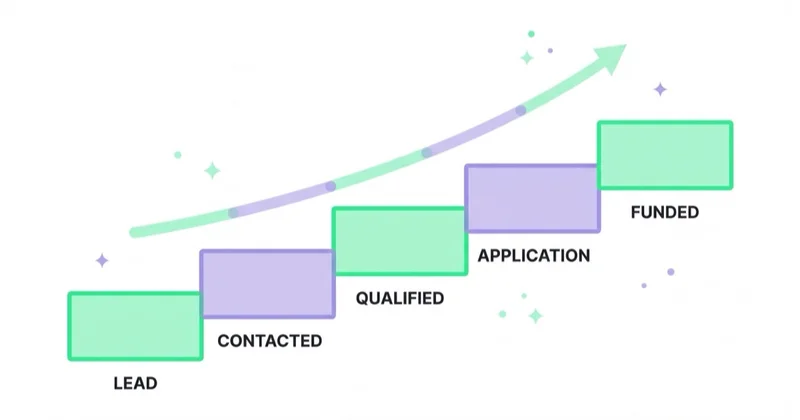

Measurement: from lead to funded loan

Cost per lead is an incomplete metric for mortgage campaigns. It can be useful for diagnosing front-end efficiency, but it can also hide major channel differences.

A better measurement ladder is:

- Click or ad engagement.

- Form, call, chat or lead form.

- Contacted lead.

- Qualified borrower scenario.

- Application started.

- Application submitted.

- Pre-qualification or pre-approval workflow milestone, where applicable.

- Locked loan or active file.

- Funded loan.

- Loan value, margin or commission proxy.

The reporting should compare channels by stage conversion, not just top-of-funnel lead cost. A channel with a higher cost per lead can win if it creates better funded-loan economics. A cheaper channel can still be valuable if it is handled as a nurture asset and not judged like immediate Search demand.

At sufficient volume and with the right consent and privacy controls, offline conversion imports can help bidding systems optimize toward qualified applications or funded loans instead of raw lead submissions. The same principle is explained in the guide to Smart Bidding strategies.

SEO and local trust for mortgage lead generation

Paid media works better when the brand is easy to verify. Mortgage prospects often research the loan officer, licensing, reviews, location and educational content before committing to a call.

Useful organic assets include:

- local loan-officer or branch pages;

- loan-type pages for FHA, VA, jumbo, DSCR, non-QM and refinance scenarios;

- first-time buyer education;

- pages explaining documents, timelines and common milestones;

- compliant FAQ sections;

- comparison pages written without misleading claims;

- Google Business Profile quality where allowed and relevant;

- partner content with real estate agents, builders or financial professionals.

SEO should not publish generic rate commentary without compliance review. The strongest organic content answers borrower questions, explains process and routes prospects to the right next step without implying individualized eligibility or a specific outcome.

Space Ads operating approach

At Space Ads, regulated lead generation is audited as a full revenue system: channel intent, compliance, tracking, CRM quality and sales follow-up. Across daily reviews of 25+ client accounts and roughly 14M monthly data points analyzed through Space Ads OS, the pattern is consistent: mortgage accounts usually need cleaner segmentation and deeper outcome tracking before scaling spend.

The operating model starts with the loan scenarios the business actually wants: purchase, refinance, VA, FHA, investor, jumbo, self-employed, local loan officer demand or partner-driven demand. Then campaigns are separated by intent, landing pages are reviewed for disclosure and message match, Meta is configured for compliant lead capture or nurture, and CRM stages are used to identify which traffic becomes funded business.

When a mortgage account reports lead volume but cannot explain funded-loan source quality, a marketing audit is the right starting point. Ongoing acquisition and measurement sit under performance marketing, with channel work across Google, Meta, landing pages and CRM feedback.

30-day action plan

- Define the loan scenarios and markets the business wants to grow.

- Review platform policy, licensing, disclosures and compliance approval workflow.

- Split Google campaigns by loan type, borrower scenario, geography and transaction type.

- Build negative keyword lists for jobs, calculators, servicing, unrelated credit products and out-of-market traffic.

- Create or update landing pages with compliant disclosures, process clarity and source tracking.

- Configure Meta as a Special Ad Category where required and review permitted targeting options.

- Separate Meta lead-form campaigns from landing-page and retargeting campaigns.

- Route every lead into CRM with source, campaign, loan scenario and assigned owner.

- Measure contacted, qualified, application, funded and lost-reason stages.

- Hold weekly lead-quality reviews between marketing, compliance and loan officers.

Common mistakes

| Mistake | Better approach |

|---|---|

| Comparing Google and Meta only by lead cost | Compare contacted, qualified, application and funded-loan rates |

| Bidding on broad mortgage terms without structure | Segment by loan type, scenario, geography and intent |

| Making unclear rate or payment claims | Send every rate, APR, fee and payment statement through compliance review |

| Treating Meta leads like active Search leads | Use education, nurture and faster multi-touch follow-up |

| Asking too much in social forms | Keep early forms lighter and move sensitive details to secure workflows |

| Tracking only form fills | Connect campaigns to CRM stages and funded-loan outcomes |

| Hiding disclosures | Keep required disclosures clear and immediately visible |

| Ignoring local trust | Strengthen loan-officer pages, reviews, local content and partner proof |

FAQ

What is mortgage lead generation?

Mortgage lead generation is the process of attracting and qualifying prospective borrowers for purchase loans, refinancing or specific loan scenarios. It includes Google Ads, Meta Ads, SEO, local visibility, landing pages, call tracking, CRM follow-up, compliance review and reporting from lead to funded loan.

Is Google Ads or Meta better for mortgage leads?

Google Ads is usually stronger for active search intent, such as loan-type, refinance or local loan-officer searches. Meta is stronger for education, early-stage demand, retargeting and lead nurturing. The better channel depends on funded-loan outcomes, not lead cost alone.

Can mortgage advertisers use Meta lead forms?

Meta lead forms can be used when the campaign follows Meta's Advertising Standards, Special Ad Category requirements where applicable, age restrictions, disclosure obligations and privacy rules. Mortgage campaigns should avoid requesting unnecessary sensitive financial information in the ad environment and should route leads into a compliance-reviewed follow-up workflow.

What compliance issues matter in mortgage ads?

Common risk areas include rate and APR claims, payment examples, fees, fixed versus variable terms, government-affiliation language, licensing disclosures, refinancing or modification claims, fair-lending requirements and privacy/consent language. Campaigns should be reviewed by qualified compliance owners before launch.

What should a mortgage landing page include?

A mortgage landing page should match the loan scenario, identify the licensed entity where required, explain the next step, show compliant disclosures clearly, provide phone and form options, set expectations for follow-up and avoid misleading rate, payment or approval language.

How should mortgage lead generation be measured?

The most useful metrics are contacted lead rate, qualified borrower rate, application starts, applications submitted, funded loans and funded-loan value. Cost per lead is secondary because it does not show whether the lead became real business.

In short

Mortgage Lead Generation performs best when Google, Meta, SEO, landing pages and CRM follow-up are treated as one regulated acquisition system. Google captures active intent. Meta supports education, retargeting and earlier-stage leads. Compliance determines what can be said. CRM data determines what should be scaled.

The strongest accounts optimize toward qualified applications and funded loans, not cheap forms. That requires clean segmentation, visible disclosures, careful rate language, fast follow-up and a feedback loop between marketing, compliance and loan officers.

Sources

- Google Ads Policy Help - Financial products and services

- Google Ads Policy Help - Restricted targeting in personalized advertising

- Meta Transparency Center - Advertising Standards

- eCFR - 12 CFR Part 1014: Mortgage Acts and Practices - Advertising (Regulation N)

- Google Ads Help - Keywords in Search Network campaigns

- Google Ads Help - Call reporting

Continue learning

- Facebook lead ads: what they are and how to launch instant forms

- Insurance agency marketing and lead generation

- Real estate agent marketing: PPC and lead generation for realtors

- Call tracking for PPC and lead generation

- Negative keywords in Google Ads: cut wasted spend

- What is a landing page and how to build one

Continue reading

Hotel and Hospitality Marketing: Direct Bookings via Google and Meta

Hotel and hospitality marketing should increase profitable direct bookings, not only booking volume. This guide covers Google Hotel Ads, Performance Max for travel goals, Meta, booking engines, rate competitiveness, remarketing and value-based measurement.

Hair and Beauty Salon Marketing: Google and Meta Ads

Hair and beauty salon marketing should generate booked appointments, rebooked clients and recurring value. This guide explains how to connect Google, Meta, Instagram, local SEO, service pages, reviews, booking systems and retention.

Restaurant Marketing: Google, Meta and Local Demand

Restaurant marketing should not be judged by likes, reach or a blended ROAS screenshot. A restaurant needs local discovery, persuasive food creative, accurate booking and order tracking, and campaigns separated by table reservations, delivery, takeaway, events and repeat visits.