Insurance agency marketing should not be optimized for the cheapest lead. A form submission can be a serious buyer ready to bind auto coverage, a homeowner comparing limits, a business owner who needs liability coverage, or a low-intent shopper who will never answer the phone. In the ad platform, those contacts can look identical. In the agency's book of business, they are completely different.

The business goal is a bound policy, premium value, commission, renewal, cross-sell and long-term client relationship. That changes the entire strategy. Google Search captures active quote and coverage intent. Meta can support education, remarketing and local trust. Customer data can improve exclusions, renewals and cross-sell when policy and consent requirements are met. CRM feedback tells the ad platforms which leads became real policies instead of letting them optimize toward easy forms.

TL;DR

- Insurance agency marketing should measure cost per bound policy. Cost per lead is only an early indicator.

- Google usually captures higher-intent demand. Search works well for product and location queries such as auto insurance quote, home insurance agency, business liability insurance or life insurance advisor.

- Meta is better for education, reminder and retargeting. It should not be treated as a direct substitute for high-intent Search.

- Life events are a content and offer strategy, not a targeting shortcut. New home, new car, new business, family changes and travel can shape landing pages and messages, but targeting must be reviewed against platform rules and local law.

- First-party data is powerful only when compliant. Customer Match, CRM lists and lookalike-style strategies need consent, privacy disclosures, platform eligibility and product-category review.

- Compliance is part of performance. Financial-services policies, insurance licensing rules and truthful claims shape what can be said in ads and on landing pages.

Why Insurance Marketing Is Different

Insurance has high competition, uneven lead quality and regulated messaging. It also has renewal value. That combination makes shallow lead generation dangerous.

First, product economics vary. A lead for personal auto, homeowners, commercial general liability, fleet, life, health, travel or group benefits does not have the same value or sales process. A single blended CPA can hide which products actually create profit.

Second, trust matters. The prospect may compare coverage, price, exclusions, carrier reputation, agent credibility, response speed and local knowledge. A landing page that only says "get a quote" often fails because it does not explain why this agency is worth contacting.

Third, many insurance leads need follow-up. A high-intent Search lead can still need documents, vehicle details, business classification, prior coverage, loss history or a needs conversation. A Meta lead usually needs even more qualification and nurture.

Fourth, insurance advertising is policy-sensitive. Google treats financial products and services as a category that requires transparency and compliance with local regulations. Messaging should avoid exaggerated savings claims, hidden conditions, misleading guarantees or unclear disclosure of who offers the product.

Segment Products Before Buying Leads

An insurance agency may sell many lines, but ads should not push them into one funnel.

| Product Line | Search Intent | Measurement Priority |

|---|---|---|

| Auto insurance | Quote, renewal, local agent, new driver | Bound policy, premium, bundle potential |

| Homeowners insurance | New home, mortgage, renewal, local agent | Policy value, home-auto bundle, renewal |

| Renters insurance | Apartment, lease requirement | Volume, low-friction bind, cross-sell |

| Life insurance | Term, family protection, advisor | Qualified consultation, policy type, long-term value |

| Commercial insurance | General liability, professional liability, workers comp | Business fit, quote quality, close rate |

| Fleet or trucking | Commercial auto, cargo, fleet coverage | Qualification, risk profile, premium value |

| Health or benefits | Group benefits, supplemental coverage | Compliance review, consultation quality |

| Travel insurance | Trip coverage, international travel | Policy value, timing, partner opportunities |

Each line deserves its own keyword groups, negative keywords, landing page, qualifying questions, value model and compliance review. A lead for "cheap car insurance" should not teach the account to bid the same way as a commercial liability lead.

Google Ads for Insurance Agencies

Google Search is usually strongest when the prospect already has a need. Examples include:

- car insurance quote [city];

- independent insurance agent near me;

- home insurance agency [city];

- business liability insurance quote;

- workers compensation insurance for contractors;

- life insurance advisor;

- insurance broker for small business;

- commercial auto insurance.

The account should separate:

- brand searches for the agency name;

- local agency searches;

- product-specific quote searches;

- commercial lines;

- personal lines;

- educational or comparison queries;

- renewal and cross-sell campaigns where policy allows.

Negative keywords are important because insurance queries attract research, jobs, training, definitions, claims questions, carrier support and low-fit price shopping. Some educational searches can be valuable for SEO or nurture, but they should not consume the same budget as quote-ready terms.

Search copy should be factual. Strong ad assets usually mention product line, location, independent or carrier relationship where accurate, quote process, licensed support, response time, reviews and clear next step. Claims such as "lowest rate," "universal approval" or "save everyone hundreds" create both trust and compliance risk unless they are substantiated and properly qualified.

Meta Ads for Insurance

Meta can support insurance marketing, but expectations should be different from Search. The strongest roles are:

- local awareness for an agency or advisor;

- educational content around common coverage questions;

- quote reminders for people who visited pages or started forms;

- lead forms with qualification;

- renewal and cross-sell campaigns to eligible customer lists;

- brand trust through team, office, review and community content.

Life-event logic can shape messages and landing pages. A new home can prompt homeowners coverage. A new car can prompt auto coverage. A growing family can prompt life insurance conversations. A new business can prompt liability coverage. The important distinction is that these scenarios should not become careless personal targeting or ad copy that implies knowledge of a private situation.

A safer creative approach is scenario-led and neutral:

- "Insurance checklist for first-time homeowners."

- "What to prepare before requesting a business liability quote."

- "Questions to ask before comparing auto coverage."

- "When to review home and auto policies together."

Meta lead forms should qualify without becoming intrusive. Ask for product interest, ZIP or service area, preferred contact method, current timing and basic context. More sensitive data should usually move to a secure quote or advisory process after consent and disclosure are clear.

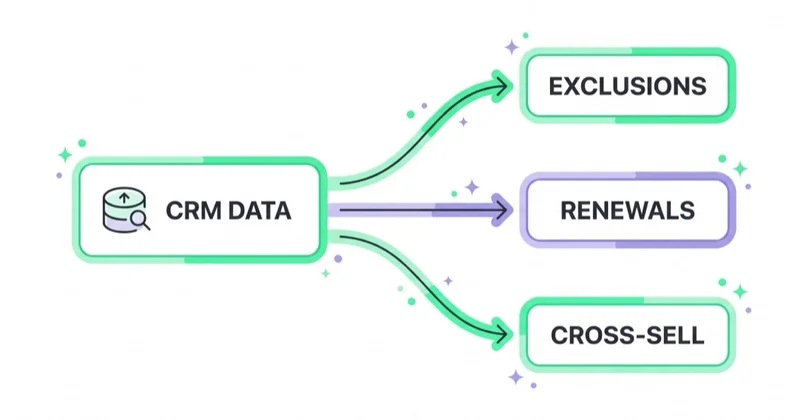

First-Party Data, Customer Match and CRM

First-party data can create a major advantage in insurance, but only when used carefully. Google Customer Match allows eligible advertisers to use customer data for reaching and re-engaging customers across Google surfaces. Google's policy requires appropriate data collection, user consent where required, accurate privacy disclosure and compliance with applicable law and platform rules.

Practical uses include:

- excluding existing clients from acquisition campaigns for the same product;

- reaching customers near renewal dates where policy and consent allow;

- cross-selling home coverage to auto clients or umbrella coverage to high-value households where appropriate;

- suppressing bound policies from lead campaigns;

- building reporting that compares source to policy value;

- feeding offline policy stages back to bidding.

The risk is assuming every list can be uploaded or used for every insurance product. Some financial, sensitive or regulated scenarios can restrict audience use. Before Customer Match, remarketing, lookalikes or CRM-based targeting are used, the agency should check consent, privacy policy language, platform rules, state rules and carrier or compliance requirements.

Compliance and Claims

This section is not legal advice. It is a marketing risk framework.

Google's financial products and services policy says advertisers promoting financial products or services must comply with state and local regulations for targeted locations and provide required disclosures. The policy also emphasizes transparency because financial products can be complex. Insurance agencies should apply that logic to ads, landing pages, lead forms and follow-up.

Common compliance checks:

- agency identity and role are clear;

- licensing information is used where required;

- carriers or affiliations are represented accurately;

- savings claims have substantiation and conditions;

- coverage claims do not overstate what a policy includes;

- quote tools explain assumptions and next steps;

- forms collect only necessary data for the stage;

- privacy policy explains advertising and analytics data use;

- remarketing and customer lists have consent and policy review;

- disclosures are visible when required, not hidden behind tiny links.

The best insurance marketing usually sounds less aggressive than generic lead-gen copy. It sells clarity, fit, speed, local support and proper comparison rather than a universal promise of lower price.

Landing Pages and Lead Qualification

An insurance landing page should not be a generic catalog of every product. It should match one intent and move the user to the right next step.

A strong landing page includes:

- product line and who it is for;

- agency role, location and licensing context where appropriate;

- carriers or markets represented, if this can be stated accurately;

- quote or consultation process;

- expected response time;

- documents or information needed for the quote;

- phone number visible on mobile;

- short form with relevant qualifying questions;

- privacy and consent language;

- reviews or local proof;

- FAQ that answers coverage and process questions without overpromising.

For auto or renters insurance, a shorter quote path may work. For commercial insurance, life insurance or more complex coverage, qualification and advisor conversation matter more. A landing page should reduce uncertainty, not pretend that every policy can be priced from one quick form.

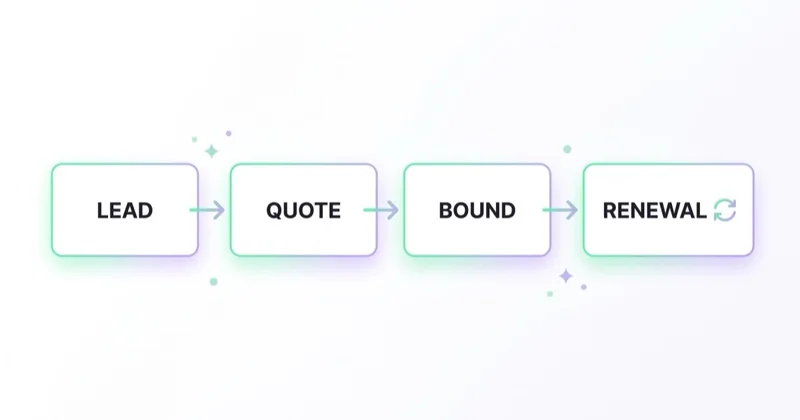

Measurement: From Lead to Bound Policy

The measurement system should follow the real sales path:

| Stage | Example Event | Why It Matters |

|---|---|---|

| Lead submitted | Form, call, lead form | Early signal only |

| Contacted | Reached by agent | Shows follow-up quality |

| Qualified | Fits product, state, timing and risk appetite | Filters weak leads |

| Quote prepared | A real quote was created | Stronger buying signal |

| Policy bound | Policy sold | Primary acquisition outcome |

| Premium or commission value | Monetary value | Needed for value-based bidding |

| Renewal | Policy retained | Shows long-term client value |

| Cross-sell | Additional policy sold | Shows multi-line value |

For Google Ads, conversion measurement, call tracking and offline conversion imports can connect ad interactions to later CRM outcomes. For insurance, this is essential because the valuable outcome often happens after a phone call or advisor follow-up, not on the website.

Call tracking should separate product line, source, campaign, qualification status and policy outcome. A lower CPL channel may be worse if it produces unqualified shoppers. A higher CPL campaign may be profitable if it creates bound multi-line policies with renewal value.

Renewals and Lifetime Value

Insurance economics depend on time. A client can renew annually, add policies, refer others or expand from personal to business coverage. That means acquisition targets should consider:

- first-year premium;

- agency commission;

- expected renewal rate;

- number of policies per client;

- bundle potential;

- commercial account value;

- service workload;

- cancellation or non-renewal risk;

- referrals and household expansion.

A simple model is better than no model. Even rough values by product line can prevent the account from treating a renters policy, personal auto quote and commercial package policy as equal conversions.

Local SEO and Trust

Many independent agencies win through local trust. Google Business Profile, reviews, local pages and advisor visibility should support paid media:

- office location and hours;

- phone number and appointment options;

- product categories and services;

- reviews and professional responses;

- team or advisor pages;

- local insurance pages by product and region;

- clear NAP consistency;

- educational FAQ content for local buyers.

Local SEO and AEO matter because prospects often ask specific questions before contacting an agent. Content such as "what documents are needed for a homeowners quote" or "business liability insurance checklist for contractors" can support both organic visibility and sales follow-up.

How Space Ads Approaches Insurance Campaigns

Across 25+ client accounts audited daily and roughly 14 million monthly data points analyzed through Space Ads OS, regulated lead-generation accounts usually fail when they optimize too early in the funnel. Cheap leads are easy to create. Bound policies with renewal value are harder to measure, but they are the real business outcome.

For insurance agencies, the Space Ads approach starts with product segmentation, compliance review, lead status mapping and CRM feedback. Then Google Search is built around high-intent product and local queries, Meta supports education and re-engagement, and first-party data is used only where policy and consent allow.

For an existing account, a marketing audit can show which channels produce bound policies and which only create cheap contacts. Ongoing execution usually connects Google Ads, Meta Ads, call tracking, CRM stages and performance marketing.

30-Day Action Plan

- Days 1-3: map products and values. Separate auto, home, commercial, life, health, travel, fleet and benefits by value and sales path.

- Days 4-7: review compliance. Check ad claims, disclosures, forms, privacy policy, licensing language and carrier references.

- Days 8-12: fix tracking. Track calls, forms, contacted leads, qualified leads, quotes, bound policies, premium value and renewals.

- Days 13-18: rebuild Search. Split product lines, brand, local terms and high-intent quote queries. Add negative lists.

- Days 19-24: rebuild Meta. Use neutral education, local trust, retargeting and qualified lead forms. Avoid implying personal circumstances.

- Days 25-30: connect CRM feedback. Compare CPL, qualified lead rate, quote rate, bound-policy rate, premium and renewal value by source.

Common Mistakes

| Mistake | Better Approach |

|---|---|

| Judging campaigns by cost per lead | Measure cost per bound policy and renewal value |

| Mixing all insurance products in one campaign | Segment by product line, value and sales process |

| Using aggressive savings claims | Use substantiated, qualified and compliant claims |

| Treating Meta leads like Search leads | Use Meta for education, retargeting and qualified nurture |

| Uploading lists without policy review | Check consent, privacy language, Customer Match rules and local law |

| Optimizing for form fills only | Import CRM stages and policy outcomes |

| Ignoring local trust | Improve reviews, Google Business Profile and local service pages |

FAQ

What is the best marketing strategy for an insurance agency?

The best strategy separates product lines, captures high-intent Google searches, uses Meta for education and re-engagement, builds local trust, and measures leads through quote, bound policy, premium value and renewal. Cost per lead alone is not a reliable success metric.

Are Google Ads or Meta Ads better for insurance agents?

Google Ads is usually stronger for active quote and coverage intent. Meta is useful for education, reminder campaigns, retargeting and qualified lead forms. Most agencies need both, but the channels should be measured differently.

Can insurance agencies use Customer Match?

Customer Match can be useful for exclusions, renewals and cross-sell when the account, data source, consent, privacy policy and product category meet Google policy and legal requirements. It should be reviewed before use, especially in regulated financial or sensitive scenarios.

What compliance rules apply to insurance advertising?

Insurance advertising should comply with platform financial-services policies, local insurance laws, licensing requirements, carrier rules and privacy obligations. Claims should be truthful, clear, substantiated and not misleading. Legal or compliance review is appropriate for specific campaigns.

How should insurance marketing ROI be measured?

Measure cost per qualified lead, quote, bound policy, premium value, commission, renewal and cross-sell. A channel with higher lead cost can be better if it binds more policies or produces higher-value clients.

What should an insurance landing page include?

It should include the product line, agency role, service area, quote process, response time, phone number, short qualifying form, privacy language, reviews and clear next steps. Complex products should usually lead to an advisor conversation rather than an over-simplified quote promise.

In Short

- Insurance agency marketing should optimize for bound policies, renewals and client value.

- Google captures high-intent demand; Meta supports education, local trust and retargeting.

- First-party data can help, but only with consent, privacy disclosure and policy review.

- Compliance is not a side note. It shapes claims, targeting, disclosures and forms.

- CRM feedback and offline conversion imports are the difference between cheap leads and profitable policy growth.

Sources

- Google Ads Policy - Financial products and services

- Google Ads Policy - Restricted targeting in personalized advertising

- Google Ads Help - About Customer Match

- Google Ads Policy - Customer Match policy

- Google Ads Help - About conversion measurement

- Google Ads Help - About offline conversion imports

Continue Learning

- Mortgage lead generation: Google and Meta for loan officers

- Customer Match in Google Ads: what it is and how to use it

- Meta Advantage+: what it is and how it works after the changes

- Facebook lead ads: what they are and how to launch instant forms

- Call tracking for PPC and lead generation

- Google Ads for local businesses, home services and contractors

Continue reading

Hotel and Hospitality Marketing: Direct Bookings via Google and Meta

Hotel and hospitality marketing should increase profitable direct bookings, not only booking volume. This guide covers Google Hotel Ads, Performance Max for travel goals, Meta, booking engines, rate competitiveness, remarketing and value-based measurement.

Hair and Beauty Salon Marketing: Google and Meta Ads

Hair and beauty salon marketing should generate booked appointments, rebooked clients and recurring value. This guide explains how to connect Google, Meta, Instagram, local SEO, service pages, reviews, booking systems and retention.

Restaurant Marketing: Google, Meta and Local Demand

Restaurant marketing should not be judged by likes, reach or a blended ROAS screenshot. A restaurant needs local discovery, persuasive food creative, accurate booking and order tracking, and campaigns separated by table reservations, delivery, takeaway, events and repeat visits.